Benefits of Buying Insurance Policies Online in India

Introduction

The decision to buy insurance is often delayed. This is not because people don’t see the need for it but because they assume that the process is too complicated and time-consuming. Today, there are no long forms, multiple visits or tons of paperwork. Just a few clicks and individuals can understand, compare and choose the right coverage. Looking for an insurance policy online offers convenience, better control and complete information.

In this blog, we will discuss the benefits that make it clear why more people now prefer to buy insurance online rather instead of going the traditional way.

- Easy Comparison Without Pressure

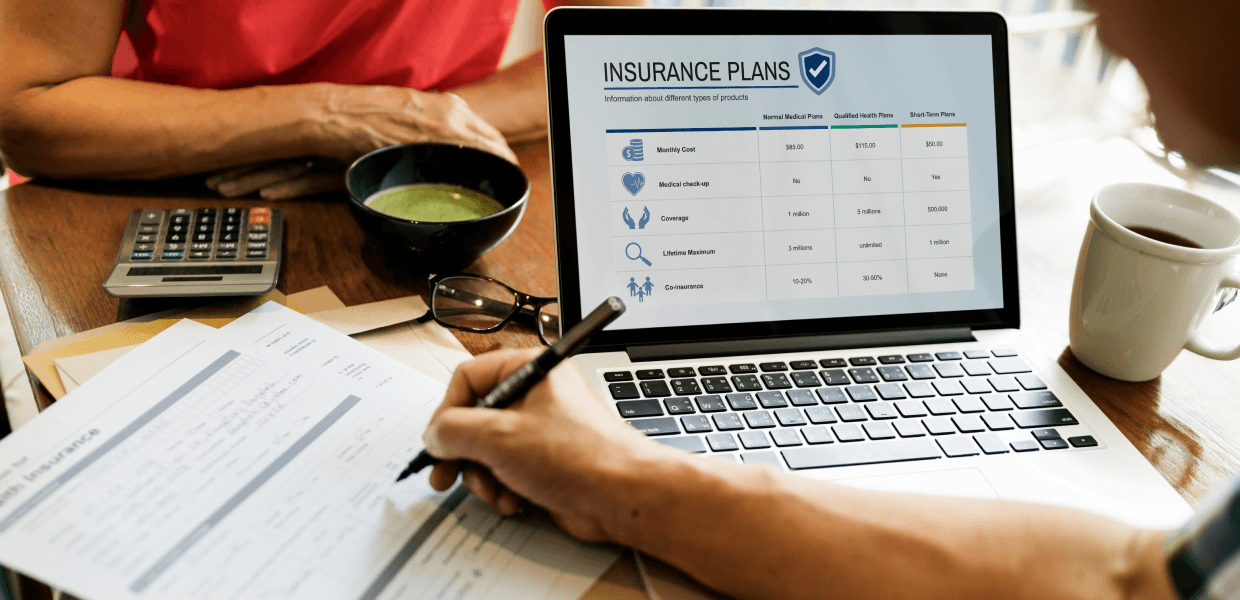

One of the best things of online insurance is that you can easily compare plans side by side. When you prefer to buy insurance online, you can:

- Compare premiums, coverage and features of multiple options

- Read policy details at your own speed and convenience

- Make decisions without anyone putting sales pressure

Finally, are able to choose a suitable policy and not the one that is pitched and pushed to you.

- Better Understanding of What You’re Buying

When explained in a very technical way or in a hurry, insurance can feel complicated. But when you switch to online platforms you can:

- Know the benefits in simple language

- Be clearly aware of inclusions and exclusions

- Understand how a term plan or other policies work

Eventually, it helps you take better decisions and you face fewer surprises later.

- Often More Cost-Effective

Exploring options and making a purchase online can reduce the extra costs because:

- There are no middlemen commissions

- Operational expenses are lower

- You get direct pricing from insurers

As a result, there are high chances of getting better premiums for the same insurance policy.

- Flexibility to Buy as Per Your Schedule

The ease around buying online insurance is that you don’t need to adjust around working hours or waste half of your day when you’re already too busy. You can simply:

- Explore plans anytime that’s suitable

- Complete your purchases from home

- Access all the policy documents digitally

This is particularly very useful for those who juggle work, family and finances together and need to specially take out time from things.

- Faster Issuing of Policy

The standard physical insurance processes can take anywhere between some days to weeks. But when you buy insurance online:

- You can submit proposals instantly

- Verification happens quicker

- Takes just some hours to issue policies

In situations when you need coverage urgently, online is always the best.

- Transparency in Premiums and Benefits

Online platforms give the clear details of:

- Exact premium breakdowns

- Insurance coverage limits

- Cost of the add-ons

Since there’s hardly any room for hidden charges, online insurance is surely a very safe option for first-time buyers.

- Easy Access to Policy Documents

Most people are anxious that they might lose the physical documents. But with online purchases:

- Policies are digitally stored

- You can access the documents anytime

- It’s easier to track renewals and updates

The long-term management of your insurance policy becomes a lot simpler.

- Simple Renewals and Updates

It’s usually a straightforward process of renewing or updating a policy online. You can:

- Renew it with a few clicks

- Update personal details quickly anytime

- Adjust coverage when you need to

With this, you can make sure that your policy remains active without any unnecessary hassle.

- Ideal for Term Insurance Buyers

You can understand the best about term plan when you can clearly see:

- What’s the coverage amount

- Duration of the policy

- Premium structure

With online platforms, these details are easy to compare. Buyers can use this information for choosing sufficient protection confidently.

- Informed Decisions, Not Impulse Purchases

When you decide to buy insurance online, you will have enough time to:

- Read the details

- Compare the options

- Think about it

There are very less chances of taking impulsive decisions. You’ll have more confidence in the policy you select.

What to Check Before Buying Insurance Online

It’s pretty simple to buy insurance online. All you need is a quick review of the important details to make sure the insurance policy works how you expect it to. The key is to focus on clarity than just cost when you buy insurance online.

- Coverage and exclusions – Super important to know what’s included and what’s not

- Sum insured and tenure –The coverage and duration should ideally match your needs, particularly for a term plan

- Claim process – Properly verify how claims are filed and supported when needed

- Personal details – Confirm if the name, date of birth and nominee information is correct

- Premium breakup and renewals – Understand the charges involved and how renewals work

Just pay attention to these careful during online insurance purchase for a reliable and stress-free choice.

Conclusion

It’s not just the technology that has influenced the shift toward online insurance. It’s actually how empowered you feel while making a decision. When you buy insurance online, you get full control, clarity and a lot of convenience.

For choosing your first insurance policy or simply reviewing a term plan, doing it online lets you make the right decisions whenever you are ready and confident and not under any pressure.